Global Coconut Derivatives Market – Trends, Drivers & Strategic Insights

Published Date : 05-Dec-2025 |

The global coconut derivatives market is forecast to grow from approximately USD 28.66 billion in 2025 to USD 54.08 billion by 2032, reflecting a strong compound annual growth rate (CAGR) of 9.5% across the period.

This expansion underscores the increasing importance of coconut-based raw materials across food & beverage, personal care, and industrial segments.

For market research firms, investors, and strategic planners, the coconut derivatives space offers a compelling mix of underlying supply-chain complexity, consumer-driven value shifts (plant-based, natural, sustainability) and regional leadership (notably Asia-Pacific).

Market Definition & Scope

“Coconut derivatives” comprise processed products derived from the coconut (Cocos nucifera) – notably coconut oil, milk, cream, water, desiccated coconut, coconut sugar, flour & fibre derivatives, and other processed fractions.

The segmentation in the referenced report covers:

- End-user: Industrial, HoReCa (hotel/restaurant/catering), Retail.

- Retail type: Supermarkets/Hypermarkets, Online/E-commerce, Convenience/Grocery, Specialty/Gourmet.

- Packaging: Bottles, Pouches/Tetra Pak, Tubs/Jars, Cans & Others.

- Product-type: Coconut oil, milk, water, desiccated, sugar, flour & fibre, other.

- Geography: North America, Europe, Asia Pacific, LAMEA (Latin America, Middle East & Africa) with country-level breakdowns.

Key Market Drivers & Trends

Plant-based & Natural Products Surge

The shift in global consumer behaviour toward plant-based diets, “clean” or minimally processed ingredients, and natural personal-care formulations has elevated demand for coconut derivatives. “Rising global demand for plant-based and natural products” is explicitly cited as a major driver.

Application Expansion Across Food, Beverage & Personal Care

Coconut derivatives are infiltrating multiple sectors: in food & beverage (e.g., coconut water, milk/cream, dairy alternatives), personal & beauty care (virgin coconut oil, coconut-based hair and skin care), and industrial uses (activated carbon from shells, coir fibre from husks).

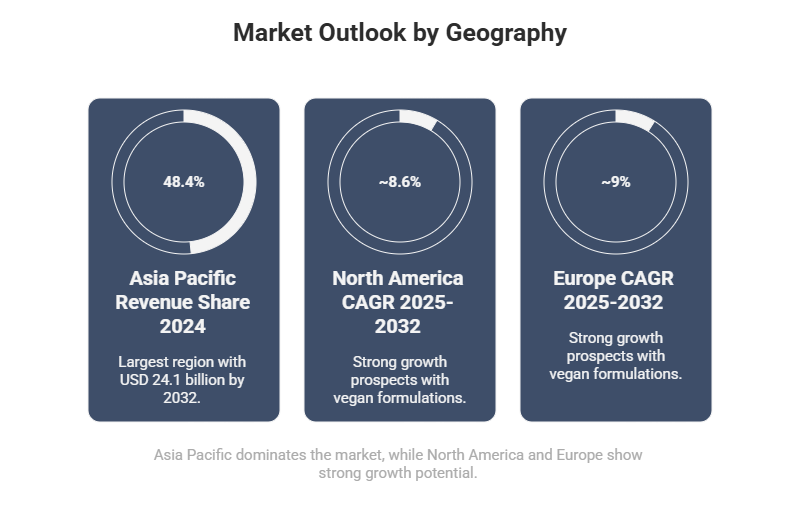

Geographic Supply Strength & Value-addition in Asia Pacific

The Asia Pacific region held ~48.4% revenue share in 2024 and is expected to maintain leadership through 2032.

Suppliers in India, Indonesia, Philippines and Sri Lanka are upgrading processing capacities and branding of coconut derivatives, increasing value-added exports.

Packaging & Retail Format Innovation

Packaging formats are evolving: bottles dominate in terms of value (26.4% revenue share in 2024) and are expected to remain dominant through the forecast.

Pouches/Tetra Pak are also gaining ground thanks to their portability and shelf-life benefits.

Sustainability & Traceability as Competitive Levers

Coconut derivative producers and users are increasingly emphasising sustainable sourcing, ethical supply chains, farmer welfare and product traceability. These are becoming key differentiators among companies.

Key Restraints & Market Challenges

- Supply-chain vulnerability: The coconut value chain is exposed to climate change, biological risks (disease/pests) and harvest instability.

- Substitute competition: Other vegetable oils and alternative ingredients may erode the share of coconut derivatives in some applications.

- Standardisation & quality assurance difficulties: Aligning supply across smallholder farms, global buyers and industrial users remains a challenge.

- Balancing multi-use of raw material: Coconuts feed multiple derivative chains (oil, water, sugar, fibre) creating allocation and cost pressures.

Market Segmentation Highlights

By End-User

The industrial segment dominated the market in 2024, capturing 51% of revenue share.

Consider that industrial applications (food processing, personal care manufacturing, activated carbon) tend to command larger volumes and longer contracts compared to retail and HoReCa.

By Packaging

The bottles format held ~26.4% share in 2024 and is forecast to remain dominant through 2032.

This reflects the dominant liquid derivative segments such as coconut water or oil and the consumer preference for transparent, portable formats.

By Geography

- Asia Pacific is the largest region (48.4% revenue share in 2024) and is projected to achieve a market size of ~USD 24.1 billion by 2032.

- North America and Europe offer strong growth prospects (CAGR ~8.6% and ~9% respectively from 2025-2032) as natural/vegan formulations advance.

Explore our full-length report for deeper insight into company strategies, value-chain mapping, country-level breakdowns and competitive landscape in the coconut derivatives market.

Strategic Implications for Market Research & Industry Stakeholders

- Emerging Market Entry Opportunity: Suppliers in coconut-rich countries (India, Indonesia, Philippines) should evaluate product-upgrading strategies (virgin oil, coconut water, fibre derivatives) and target export markets via value-added branding.

- Retailers & Brand Owners: Brands can capitalise on the “natural + plant-based” trend by leveraging coconut derivatives in formulation claims, sustainable sourcing messaging and premiumisation.

- Packaging Innovation: As consumer convenience and on-the-go hydration continue to rise, tracking packaging formats (light-weight bottles, pouches) becomes critical.

- Supply-Chain Analytics: For analysts, monitoring coconut yields, plantation renewal, smallholder productivity and trade flows provides forward-looking signals for derivative pricing and margin pressures.

- Competitive Intelligence: Key players profiled include Marico Limited, Cargill, Incorporated, Wilmar International Ltd and others. Market-research professionals should track M&A, partnerships, sustainability initiatives and product launches among these.

- Regional Strategy: For investors and strategic planners, Asia-Pacific offers scale and raw-material strength, while Western markets offer demand growth for premium/clean label derivatives.

Outlook & Conclusion

The coconut derivatives market stands at an interesting intersection of supply-rich geographies, shifting consumer demands toward plant-based and natural ingredients, and industrial applications expanding beyond traditional food oil. With a projected CAGR of 9.5% from 2025 to 2032, the market is set for robust growth.